I appreciate Mr. Webster bringing risk calculation methodology to the forefront for discussion. The focus of my article was limited to the overall processes of analysis rather than specifics. The very character of risk is an excellent topic in further exploration of these important concepts and principles.

Mr. Webster contrasts positional risk - determined using distance in space as I suggested in my article on traditional risk - calculated using a simple product of consequence and probability (which I will refer to as actuarial risk because it merely expresses risk as cost-over-time).

I first emphasize that both risk calculation methods have value and place. In fact, my intent is to supplement rather than supplant actuarial risk. It is important to understand the value and how each method should be used. There is no correct or incorrect method, rather better and poorer applications for each.

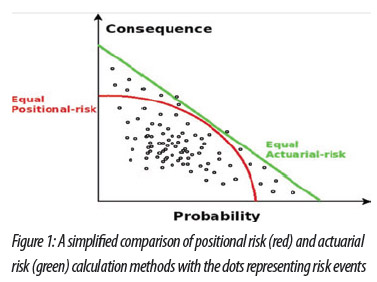

Mr. Webster suggests that using positional risk is synonymous to simply adding voltage and current to get power (wattage) for a motor. In fact, Euclidean distance is more closely related to the product of the components than to the sum and most importantly incorporates the fact that consequence and probability are two very different characterized contributors to risk. Positional risk is a "planer" calculation rather than a linear one. Think of consequence as a north-south value, while probability is an east-west value, with positional risk being distance over the landscape. Figure 1 shows a simplified comparison of constant risk lines using positional risk and actuarial risk calculation methods along with points for many risk events one might encounter within a real system represented as dots.

For an electrical motor, wattage is certainly a limit for the motor in many ways. However, it is not the ONLY limitation. Voltage limits exist that are based on insulation capabilities. On the other hand, amperage limitations are based on heat dissipation capabilities - quite different characteristics and also different from those associated with wattage limits, such as shaft torque, etc. Hypothetically, even with extremely low voltage applied to a motor, high current could damage the motor even though the total wattage is far below acceptable levels. Similarly, extremely high voltage could damage the motor even if far below wattage limits. In a motor (any electrical circuit), we need to be concerned about outliers in respect to ANY of the three aspects: voltage, current, or wattage. Likewise, we need to identify outliers in any of the three aspects of risk: consequence, probability, or actuarial. It is easy to see in Figure 1 that positional risk identifies outliers, while actuarial risk limits outlier identification to only those based on actuarial risk.

This is further demonstrated in chart form. Figure 2 is produced using positional risk calculations. It shows that outliers along each axis (rows one and four) calculate risk values comparable with outliers in actuarial risk (row three) and greater than values for non-outliers, such as row two.

Figure 3, with the same four points as Figure 2, shows that actuarial risk calculates very low values for even extreme outliers along the axes (rows one and three) similar in value to non-outlying points such as Row 2. Only the single actuarial risk outlier is identified.

The essential aspects of identifying outliers that are closer to the axes are many, but the two most important are to avoid becoming "bean counter" driven and to find real opportunities for improvement. Actuarial risk methods likely would not have identified significantly major, but rare events, like the Bhopal disaster, the Fukushima nuclear reactor disaster, or the BP oil spill, because their extremely low probability would relegate them to obscurity. Positional risk methodology might have made all three possibilities clear and difficult to downplay. On the other end of the spectrum, extremely frequent but relatively low consequence events would also be ignored by actuarial risk, resulting in "consequence leaks" that might add up to major overall significance and multiple lost opportunities for improvement, known as pound wise and penny foolish.

Once outliers are identified using positional risk, then responsive actions can be evaluated for potential outcomes and compared to as-is or alternative cases. This is where actuarial risk is rightly applied as suggested by Mr. Webster's comparison of his cases A and B. As he suggests, a real and actual improvement in risk profile is necessary to justify making the change. We don't want to just move the problem from one of consequence to one of probability, or the other way around.

Just as actuarial risk is less valid for discriminating and prioritizing opportunities and challenges, positional risk is less valid for evaluating effectiveness of various options to address those opportunities and challenges. In essence, positional risk is the horse and actuarial risk is the cart. We should not use a cart in place of a horse, or the other way around. As we all know, we shouldn't put the cart in front of the horse.

Read Terry's original article - Risk & Criticality